Mexico’s Petroleum Hedging Program as Counter-Cyclical Insurance

For nearly two decades, the Mexican Treasury has run an insurance-like program to hedge against declines in crude oil prices, which could otherwise substantially constrain government spending. This new report from the Jain Family Institute evaluates the program, widely known as the “Hacienda Hedge” in Anglophone financial circles, drawing on twenty years of data as well as a set of Monte Carlo simulations.

Available in English, Spanish, and Portuguese, the report finds that the hedging strategy has served the Mexican government as an effective form of insurance against downturns in oil prices, improving its credit rating and protecting critical public spending while demonstrating cash-flow positivity over the lifespan of the strategy.

Critical to the success of the Hacienda Hedge, the authors find, are its simplicity, efficiency, and continuity, reflecting the Mexican Treasury’s prioritization of counter-cyclical insurance coverage over speculative bids at outsize returns. An accompanying set of simulations point to the possible stabilization effects and cash-flow positivity of similar hypothetical strategies, suggesting that such insurance-like approaches may be of relevance to a wide range of oil-exporting countries, including Brazil, where petroleum export and price stabilization policies are the subject of ongoing debate and experimentation.

Read the report in English here.

Related

Mineral Wealth and Electrification — Technical Appendix

On data sources and data processing.

Part of the series Mineral Wealth and Electrification

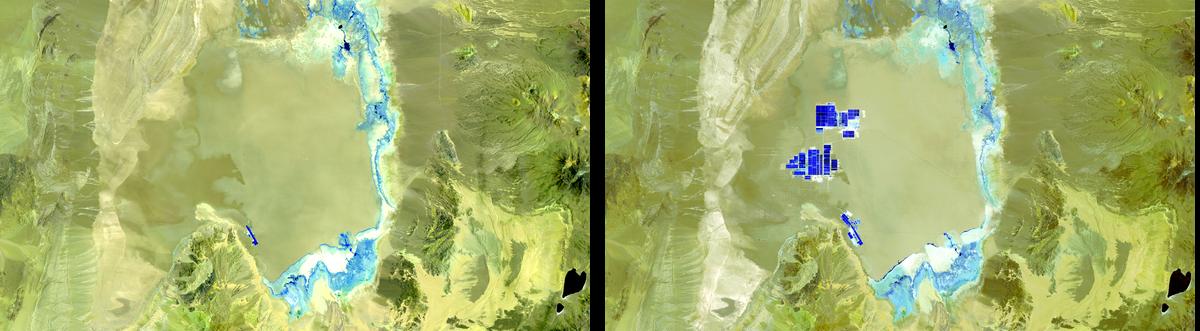

Mineral Wealth and Electrification — Report

This report adopts a producer-country perspective centered on the potential for wealth creation and public value capture and investment.

Part of the series Mineral Wealth and Electrification

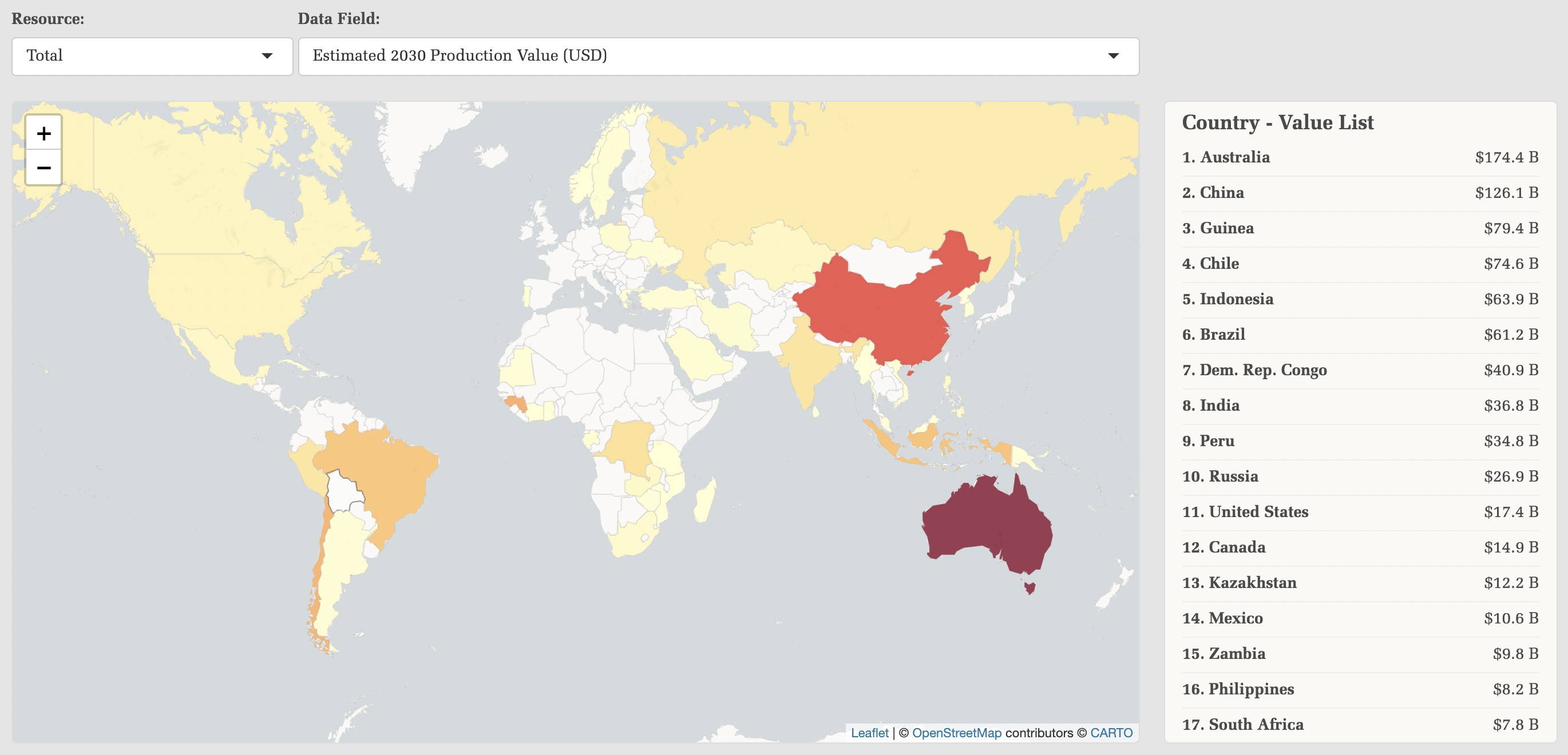

Transition-Critical Minerals: Wealth Endowments and Value Capture — Interactive Map

A high-level distribution of current and future mining production and potential royalty revenue globally through 2030.

Part of the series Mineral Wealth and Electrification